The Rich Mind Blog

Understanding Liquidity

Consider your assets as they are invested today, and determine where they fall on the spectrum of liquidity.

If most of your money is in your retirement plan (less liquid), and you have a minimal amount of money in your savings account (more liquid), then you may not have enough liquidity. That’s because your retirement plan would be harder to access, and borrowing against it may cause a penalty. In comparison, your savings account is easier to access, and is therefore more liquid.

So, Why is Liquidity so Important?

The Problem:

Most people don’t have enough in more-liquid savings.

Two-thirds of Americans say they would struggle to come up with just $1,000 to cover an unexpected expense.1 Even 38% of people who make more than $100,000 per year say they would have some difficulty coming up with the $1,000.1 Regardless of income level, most people don’t have enough liquid savings — so an unexpected expense may result in financial disruption.

Have you considered how you might respond to an unexpected expense? You may have a variety of different types of accounts, but would it be possible to access that money?

The Solution:

Striking a balance between more-liquid and less-liquid assets.

Creating a balance by having a mix of more-liquid and less-liquid assets is key to being prepared to handle your todays — and your tomorrows.

Consider again how you would access your money in a bank account vs. your retirement plan.

A savings account is undeniably more liquid because you can always access your funds and receive every dollar, whereas a retirement plan is much less liquid because there may be penalties for early withdrawal. Not all assets are black and white when it comes to liquidity. It’s possible for some assets to be more liquid than others. To determine whether an asset is more or less liquid, ask yourself:

- Can I convert it to spendable money immediately?

- Will I receive the full value of my money (no penalty or financial loss)?

If the answer is “yes,” the asset is considered more liquid. If not, the difficulty of accessing your money and the extent of penalty determines that the asset would be considered less liquid.

Because mutual funds only take a few days to access and usually realize their current value, they are considered more liquid. The short wait for the full amount of your funds can be much easier than an early withdrawal from a retirement plan.

Real estate is considered less liquid because it can take months, even years, for property to be sold and converted into spendable money — and it’s possible to lose money on the sale. However, that doesn’t mean that real estate can’t ever be a good investment. That’s why having a mix of more-liquid and less-liquid assets is important.

How to Strive for a Balance

So, you’re saving 15 to 20 percent of your gross annual income. Where exactly should you put your money?

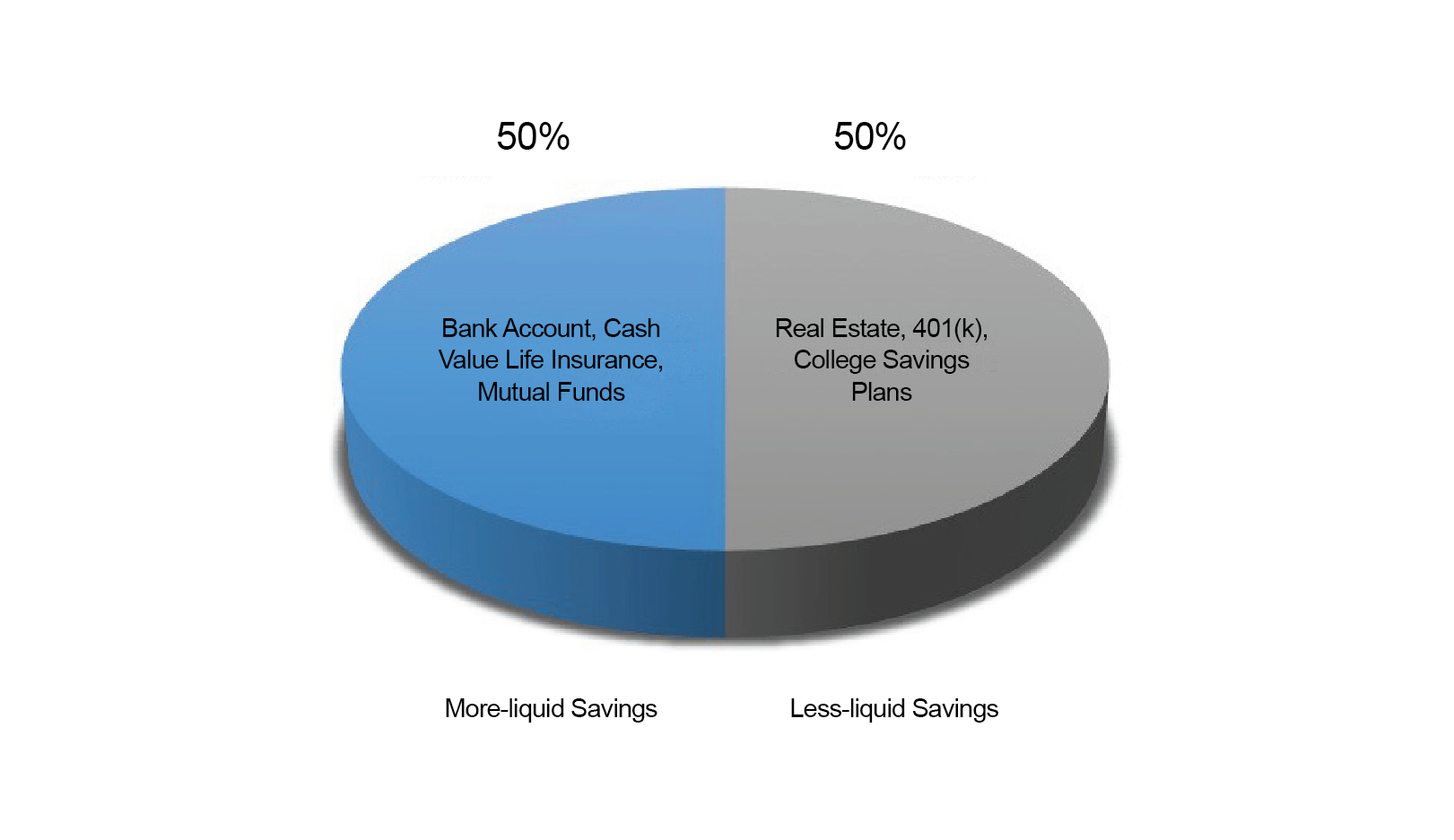

You may want to consider having 50 percent of your assets in more-liquid funds, and 50 percent in less liquid funds. This is a general guideline — everyone’s situation is unique.

But, first things first. You need liquid assets to be financially prepared for life’s unexpected events. That means you should consider building life event funds of 80 percent to 100 percent of your income in more liquid savings — money that you can access immediately. Savings accounts, mutual funds, and whole life insurance with cash value are all liquid assets that can provide the money you need to be financially prepared for today.

Once you’ve built your liquid life event funds, it’s time to consider putting your savings into less-liquid assets that can help you in the long term. Your retirement plan, college savings plans, and real estate are all assets that can provide protection and income for the future.

For example, if you have $100,000 in a retirement savings account, real estate and another $100,000 in bank accounts, mutual funds, and cash value life insurance, you are on your way to having balanced liquidity.

Your Finances, Balanced.

Savings: A mix of more-liquid and less-liquid assets

Fortunately, having a balance of more-liquid and less-liquid assets puts you well on your way to being a world-class saver2 on the path to Financial Balance®. By building life event funds with adequate more-liquid savings, and less liquid savings for the long term, you’re setting yourself up for financial confidence.1 “Views of the National Economy Are Clouded by Personal Finance and Employment Concerns.” Projects/Programs.

The Associated Press-NORC Center for Public Affairs Research, 2016

2 Guardian considers someone who saves at least 15 to 20% of their income to be a World-Class Saver.

This information is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC

is not undertaking to provide any recommendations or investment advice regarding any specific account type, service,

investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity.

Please contact a financial professional for guidance and information that is specific to your individual situation.

Share article with your network.

Focus on Your Financial Journey with

The Rich Mind Newsletter

Get finance tips and money conversations straight to your inbox!